Inflation at 9.9%. Gas prices up 450% from September 2021. The economy on the brink of a gruelling recession. These are the immediate issues Liz Truss promises to fix upon being elected leader of the Tory party. With one in every 3 children living in poverty in the UK (a figure which shows no sign of plateauing), and more people reverting to food banks to survive, it is critical that Liz delivers.

Will she be able to with her planned measures? What might be the negative impacts? Is there anything the UK can do to escape the tough times and even worse times ahead?

Energy price cap

The most recent measure implemented has been a two-year energy price cap of £2500 for households, with businesses being granted this for 6 months. This means that if (and when) energy bills exceed this, the remainder will be paid for by the government. While Kwarteng states it will only cost £60 bn, most estimates range from £100-150 bn due to estimates that gas prices could be as high as £6000 next year. Truss states the aim of this is to ensure that households can budget with the highest price of energy in mind, stripping away the uncertainty brought about by hiking prices.

With government debt standing at 99.6% of GDP, critics condemn this measure due to implications on public finances, stating they will only be paid for in the future in the form of higher taxes, especially with the recent interest rise to 2.25% which makes government borrowing even more costly. Yet, one might argue that economic policy is a game of choosing what the ‘least bad’ option is. In this case, stopping people from starving now and increasing taxes at a more stable time (even if that means slower growth) seems the sensible side to take.

Taxes

The issue arises when she reveals the other branch of her fiscal policy: cutting taxes. First, this leaves government finances even more precarious as there seems to be no plan as to how to levy the necessary revenues to finance the energy scheme – the Exchequer scorecard for the tax cuts stretches to 2026/27. Nonetheless, she has declared that she wishes to ‘put money back in the pockets of people who need it most’. But do her tax cuts to national insurance and corporation even achieve this?

Reversing the 1.25% rise in national insurance benefits people earning more than £100,000 the most, making this a regressive tax and thus an inequality broadening move. Moreover, tax cuts take a while to filter through to peoples’ disposable incomes, being more reminiscent of a medium-term plan rather than one which helps people to pay their bills and survive now.

She has also declared plans for a temporary moratorium on the green energy levy to lower bills. While this levy currently makes up 8% of energy bills, thus its removal signalling lower costs for households, the moratorium proves counterintuitive. With renewable energy companies being subsidised by this levy, the funding is helping to limit electricity price increases by reducing the need to import expensive gas. They also fund support schemes like home insulation which save vulnerable households money and are going to be essential in the coming years. Therefore, this move threatens to stunt the sector which is helping to keep costs down for consumers.

The planned corporation tax rise from 19% to 25% has been cancelled. The prime minister claims that she wants to ‘prioritise growth’ so that the entire economy can benefit. The theory goes that by cutting taxes more people will invest in UK businesses who will in turn become wealthier and distribute their income by spending on the domestic economy. Thus, she proposes a basic case of trickle-down economics. Biden (and many others) doubt the plausibility of this theory, highlighting that rather than the desired distribution of wealth, tax cuts of this kind allow firms to pocket more of their profits. Truss meets these accusations with fervent denial but provides minimal justification as to why her logic is not trickledown.

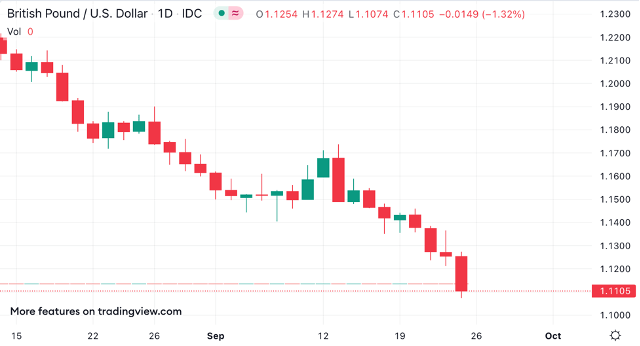

Even if her sole goal is 2.5% annual growth (no matter the social cost), that the tax changes could achieve this is highly speculative. As displayed in the chart above, the pound dropped almost vertically after the announcement of Kwarteng’s mini-budget, suggesting that investors are selling their pounds due to lack of confidence in the UK economy, despite the fact the budget was designed to increase market confidence through tax incentives and reform. Perhaps it is the lack of transparency displayed by the failure to publish an independent OBR forecast.

As such, cutting taxes in hopes of boosted investment appears speculative and long-term at best. At worst, it worsens government finances and does nothing to help those wondering where their next meal is coming from.

Inflation

Here comes inflation. The inflationary climate is cost-push and driven by supply side factors. This has led some to remark that any contractionary fiscal policy employed by Truss would be futile in achieving lower inflation. However, such blatant expansionary policy only serves to bolster the price level by increasing aggregate demand. The sheer size of these tax cuts is second only to Barber’s ‘dash for growth’ in 1972, which caused a bubble to burst and inflation to spiral.

Besides eroding the real incomes of pensioners and those on fixed incomes, what makes the fiscal policy more dangerous is the interest rate rise her policy is encouraging. By increasing the rate of inflation, the bank of England (whose sole target is to achieve a 2% inflation rate) increases interest rates in hope of lowering consumption and spending. Those who are not on fixed-rate mortgages see their mortgage bills surge, negating any positive impact of the tax cuts (which we have already revealed are minimal for lower-income households). This will not impact the top 10% who are more likely to have already paid off their houses but will bite into the depleting funds of the lower-middle-class and the poorest. The BOE’s announcement that the base rate will rise to 2.25% is not likely to be the last we hear from them, with some estimates that it may reach as high as 5%. The government’s policy is only peddling this trajectory.

Alternative measures

This low-tax approach rules more effective measures off the list, such as a windfall tax on the profits of energy companies. Such a tax targets those profiting disproportionately, whilst simultaneously allowing government to finance its deficit. For example, Rome adopted a 10% tax increase on windfall profits and raised the rate to 25% in May. The Treasury even estimated that the energy sector will make up to £170 billion in excess profits over the next two years. In the mini-budget, Kwarteng failed to justify the absence of a windfall tax.

If Truss is focusing on the long-term, she will hit a brick wall by failing to tackle the core of the energy crisis.

While the exogenous shock of the war in Ukraine has seen gas prices spike worldwide, the problem in England is unique in that the extent of the crisis has come about due to long-standing, systemic weaknesses. A decade ago, the energy industry was an oligopoly, dominated by 6 big companies who experienced huge profits. Ofgem, the regulator for this industry, increased competition, allowing 90 firms to operate. However, without necessary financial background checks, 48 of those companies have gone bust, with 29 of those being in the last year, leading to 2.7 million customers being transferred to a different supplier. This meant that to cover costs of new customers (whose energy expenditure they did not plan for), companies had to charge their existing customers more.

Thus, Truss needs to stop scapegoating with Putin and fix up regulation in the energy industry so that providers have robust finances and knowledge before entering.

Conclusion

In the short-run, the energy price freeze will seriously help. But this is about as far as her policy goes when helping those suffering the most due to the cost of living crisis. Wealth gains to the poorest via tax cuts are counteracted by interest rate rises on mortgages.

The long-run has a less binary judgement. Truss’ and Kwarteng’s efforts to boost long term growth may prove effective in the long-run – but it will certainly take time and is not looking likely as indicated by the immediate drop of the sterling following the announcement of these plans.

Even if growth of 2.5% is achieved, people in the future will not enjoy it due to the stifling taxes that will ultimately have to be put in place to finance the spending of covid and this recent spree. Time will tell.